Wealth-Tech New Co

A preliminary business plan for a new wealth-tech business

In an effort to think through prospective ideas, I occasionally go through the exercise of writing a preliminary business plan. The following is a preliminary business plan for a new wealth-tech business.

Alternatives for RIAs New Co

Mission

Empower RIAs with the tools to invest in alternatives. By automating vital tasks such as capital calls and document processing as well as facilitating portfolio curation, client communication, and access to various alternative investment types, we strive to become RIAs' comprehensive platform for alternative asset management.

Product

The master plan is broken down into four steps. I have validated steps 1 and 2 and have yet to fully validate steps 3 and 4.

1. Become the digital admin for private investments: Recognizing the struggles that RIAs often face in managing the 10-12 different point solutions they typically use, we sought to solve this problem by focusing on data integrations with an emphasis on alternative investments. Managing alternatives today involves a complicated jumble of hundreds of data sources, daily emails, manual data reconciliation, a decentralized tax process, and manual reporting. We saw this as an opportunity to streamline and simplify. Our first step is to provide seamless data integrations, with a focus on automating and predicting capital calls, document processing, and data ingestion. We transition RIAs from a fragmented system to a unified platform - one daily digest, automated data checks, a digital tax list, and digital reporting and integrations. In essence, we become the digital administrative hub for private investments, significantly simplifying the management process and enabling RIAs to focus more on their core responsibilities. I have validated that current offerings currently charge large RIAs over 7 figures to provide some of these features. The high cost positions these offerings as some of the most premium-priced point solutions in the wealth management stack.

2. Provide access: The second phase of our strategy provides access to alternative investments - encompassing real estate, venture capital, private equity, and private credit - while deploying LLMs as a critical enabler. The use of LLMs is central to our approach, enabling us to curate alternative portfolios and furnish RIAs with a powerful tool to articulate alternative offerings to their clients. Information about alternatives is typically more qualitative than quantitative. This qualitative nature of alternatives data can make it more difficult for clients and RIAs to understand and evaluate. Explaining the intricacies of a venture capital firm's portfolio of startups, for example, can involve delving into a wide range of industries, technologies, and business models. Similarly, assessing a real estate investment might require understanding local market conditions, property development plans, and regulatory issues.

Our initial approach will bundle existing private alternative access providers, such as Moonfare, CAIS, iCapital, and Allocate, based on our validated understanding that these companies are open to this arrangement and see value in us as a channel partner. Ultimately, our goal is to vertically integrate these services and facilitate access ourselves in addition to launching our own funds and liquidity solutions in order to further capitalize on carry while aggregating investor capital into a single vehicle to ensure a smooth process for fund managers. The result: a unified platform for RIAs to manage all their alternative investments, curate customized portfolios and streamline client communication.

3. Enable RIAs to become their own mini banks: Our third step aims to transform RIAs into comprehensive financial service providers, akin to their own mini banks. Recognizing the trust that clients often place in their wealth managers, over their traditional banks (just 28 percent of the millennial and Gen Z generations trust their banks), we see an opportunity to extend the RIAs' service offerings. This expansion encompasses a range of lending products, including personal loans, home equity loans, auto loans, and more, alongside insurance products such as life, car, and home insurance. We envisage achieving this either through white-labeling an underlying banking provider and empowering RIAs to offer these services directly, or by offering products from other banking providers in a marketplace model. Although fiduciary responsibilities present a potential challenge in this realm, our initial validation suggests viable workarounds exist, opening the door for RIAs to deliver a more holistic and trusted banking experience.

The retreat of banks and nonbanks from mortgage lending due to increased risk aversion and liquidity constraints has left a gap in the market that RIAs could potentially fill. This shift in the financial landscape presents a tailwind for RIAs to expand their traditional services and offer lending and insurance products, which were previously dominated by banks. With their client-centric approach and focus on long-term financial planning, RIAs could provide personalized loan services to their clients, thereby diversifying their business model. This opportunity is contingent on RIAs ensuring adequate liquidity to manage associated risks, but the current market conditions indicate a growing need for such services, providing a unique expansion opportunity for RIAs.

4. Become a next gen turnkey asset management program (TAMP): As our final step, we aim to consolidate the various point solutions in the wealth management tech stack to become a comprehensive TAMP. In contrast to traditional TAMP models, our revenue will be driven solely by transaction fees on the platform, not asset-under-management (AUM) based fees which normally hover around 0.1% - 0.5% for TAMPs. Anticipating fee compression in the coming years, we foresee our new business model, which also encompasses alternatives management, rapidly gaining traction. The scope of our TAMP will cover the gamut of wealth management services, including portfolio and performance reporting, CRM, portfolio modeling, rebalancing, direct indexing, trading, billing, financial planning, client portal management, aggregation, compliance, document management, workflow, and proposal generation. This holistic approach positions us as a single, integrated solution for wealth management, streamlining processes for RIAs and their clients.

Market

Despite alternatives gaining traction, most global savings are scarcely invested in these assets, with the average wealth advisor allocating just 0-4% of their portfolio to private investments, largely due to resource constraints and limited accessibility. Representing less than 10% of public markets, private markets ($12T global private markets AUM) remain a largely unexplored, yet expanding, opportunity.

Broader Market Opportunity:

6k+ RIAs

11k+ family offices

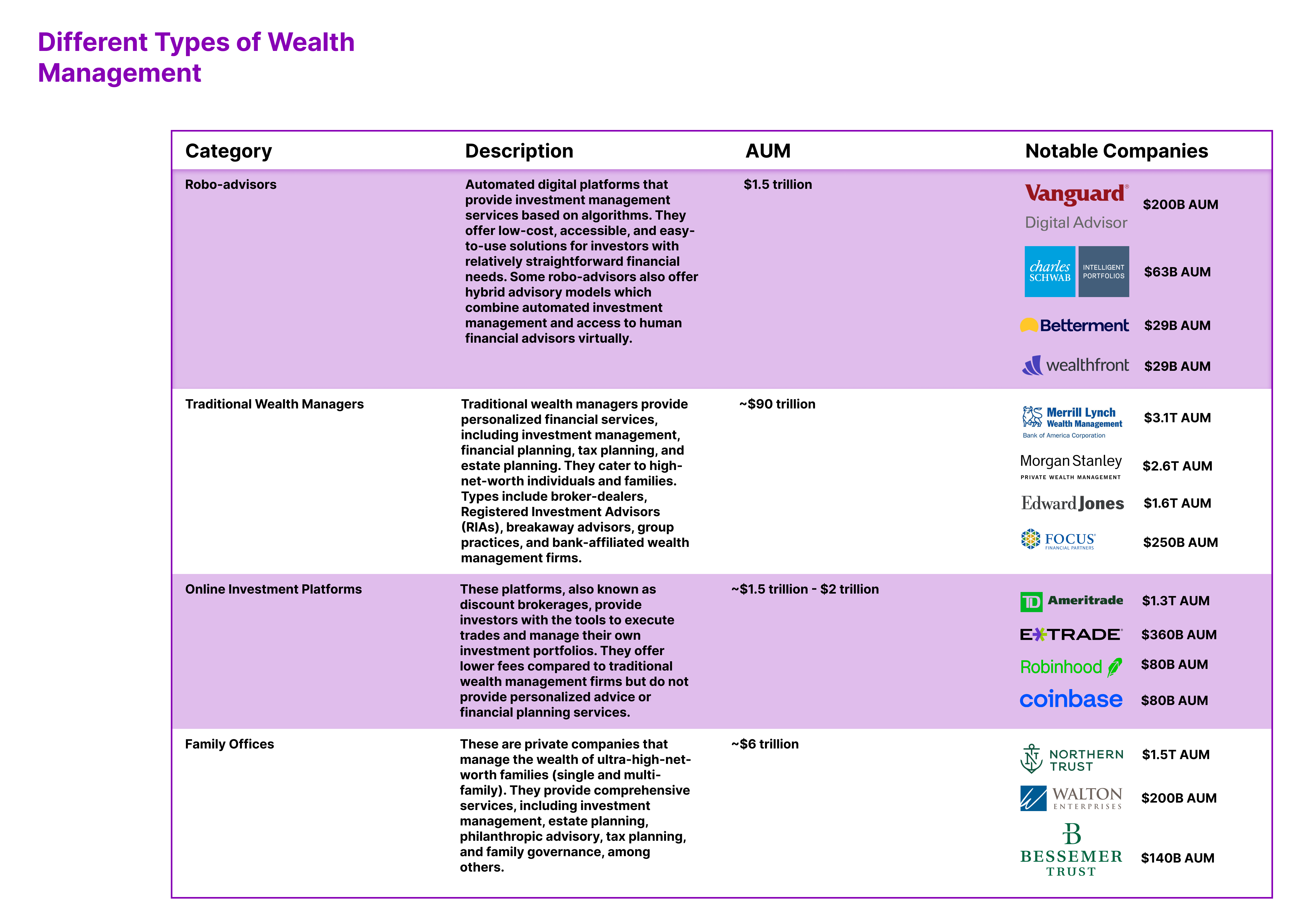

$90T+ in global private wealth

15% yearly total asset growth of RIAs despite the rise of robo-advisors

$90T * 0.5% (average TAMP fee) = $450B market size

Targeted Go To Market:

10% of advisors that are independent as opposed to bank affiliated managers (e.g. Morgan Stanley Wealth Management) and large institutional advisory practices (e.g. Edward Jones).

$285M avg firm AUM

$10T AUM * 0.5% (average TAMP fee) = $50B market size

Why Now?

The private markets are increasing in size and are projected to increase to $15T by 2025 (5x increase since 2003)

The number of publicly traded companies has reduced by 40% over the last 20 years. Companies are staying private longer.

The number of qualified LPs has increased by 5x over the past decade and $3T of retail capital is expected to move into alts by 2025

LLMs provide an unprecedented solution to help curate alternative investment portfolios and articulate offerings to RIAs and their clients

Competitors

Existing companies tend to focus either on providing access to investments or solely on document processing for alternatives (we have reason to believe that the technology behind document processing for alternatives can be easily replicated and offered more affordably). A firm that combines both these services and ultimately broadens its scope to evolve into a next-generation TAMP could carve out significant market share.

The Coaterie: Limited integrations to the rest of the wealth tech stack. Only supports access to venture funds.

iCapital: Only supports funds they facilitate access to. Limited integrations to the rest of the wealth tech stack.

Opto Investments: Only supports funds they facilitate access to. Limited integrations to the rest of the wealth tech stack.

Moonfare: Only supports funds they facilitate access to. Limited integrations to the rest of the wealth tech stack. Only supports private equity and venture.

Arch Labs: Solely document processing for alternatives. Does not facilitate access. No automated capital calls.

Canoe Intelligence: Solely document processing for alternatives. Does not facilitate access. No automated capital calls.

Allocate: Only supports funds they facilitate access to. Limited integrations to the rest of the wealth tech stack. Only supports venture funds.

Juniper Square: Does not serve wealth managers.

CAIS: Only supports funds they facilitate access to. Limited integrations to the rest of the wealth tech stack. Does not support venture funds.

Cadre: Only supports funds they facilitate access to. Limited integrations to the rest of the wealth tech stack. Only supports real estate.

Percent: Only supports funds they facilitate access to. Limited integrations to the rest of the wealth tech stack. Only supports private credit.

Risks / Objections:

1. Wealth managers are not going to exist in the future

Wealth managers will continue to play a crucial role in the financial landscape. Despite the rise of robo-advisors, the human element of wealth management has seen annual growth exceeding 15% over the last decade, reflecting the ongoing demand for professional advisory services. Most clients, particularly those with considerable assets, still value and seek this personalized guidance. Furthermore, we envision that wealth managers will increasingly serve as the conduit for clients affluent and above (see appendix figure 1) to access banking services such as loans and insurance, further solidifying their relevance in the future of finance.

2. RIAs are price sensitive. There isn’t room for a new entrant to charge an AUM fee

We agree. Our business model centers around charging transaction fees on alternative investments in addition to carry in the funds we facilitate access to which makes us financially aligned with both fund managers and RIAs.

3. Financial advisors are tech-phobic and difficult to sell to

77% RIAs cite automation and digital capabilities as their biggest need in the next 5 years

61% of advisors still spend at least 40% of their time on investment management activities

78% of clients who cite use of technology as a key factor in choosing or leaving their advisor

Easily got in front of RIAs during customer discovery and already received 7 figure pilot opportunity (soft commitment)

4. Alternatives are going to stay a velvet rope

Private equity firms have already become fairly commoditized. We see this given their focus on targeting private wealth and through their swift scaling of AUM. Total private markets AUM reached $11.7T as of last year and has grown at an annual rate of nearly 20 percent since 2017. For reference, Blackstone alone manages $881B with $241B coming from the private wealth channel (partnerships with financial advisors). Venture will most likely go this route as well. Early indicators may include A16Z, Tiger Global, Softbank, etc.

5. There is not a clear AI use case

Given their proficiency in curating alternative portfolios and explaining complex alternative investments, LLMs can serve as an invaluable tool for RIAs, aiding in both client communication and their own understanding. The nature of data in the realm of alternative investments is predominantly qualitative, encompassing narrative and descriptive elements about a company's business model, market dynamics, management team, and growth strategies, among other factors. Such qualitative data can be challenging for clients and RIAs to decipher and evaluate. Considering that most RIAs have minimal investment in alternatives (with an average allocation of under 4% and many having no allocation at all), LLMs could have a significant impact in broadening investment in alternatives. Additionally, these models can help elucidate macro trends and monitor news proactively. They can serve as a client-facing tool providing round-the-clock responses to queries, and their training can be tailored to include internal firm documents and intelligence for enhanced context understanding. LLMs can also contribute to compliance efforts (e.g. monitoring internal emails).

6. This is just not that interesting

This approach has the potential to fundamentally transform how individuals interact with essential banking services. By enabling RIAs to offer services like investment management, loans, and insurance, we're reshaping the traditional banking model. Rather than dealing with a bank, customers would engage with their trusted wealth managers for a range of financial services. If we validate this, it signifies a paradigm shift in how we interact with banking services - moving away from traditional banks towards a more personalized, trusted, and integrated experience with RIAs (it's important to clarify that our approach is primarily geared towards clients with more significant holdings).

7. There are too many competitors

While it may seem like there are numerous competitors in the space, it's important to note that many of these entities are more accurately defined as point solutions. Initially, our strategy is to bundle these solutions, offering a comprehensive suite of services to our clients. Over time, we plan to vertically integrate these services, adding value and reducing complexity for our clients.

Additionally, there exists a largely untapped niche: going directly to consumers who are currently managing alternatives on their own without the assistance of a wealth manager. This approach could extend the reach of our services, although it's worth noting that direct-to-consumer finance products in the investment management space have historically faced challenges. Hence, while this is a potential avenue, our primary focus remains on enhancing and simplifying the experience for RIAs and their clients.

Appendix

Figure 1

Figure 2